There’s been a big shift in consumer habits online when it comes to mortgages.

Data from LowestRates.ca shows that in the past two quarters (Q2 and Q3), far more consumers got quotes for five-year fixed mortgages than variable-rate mortgages.

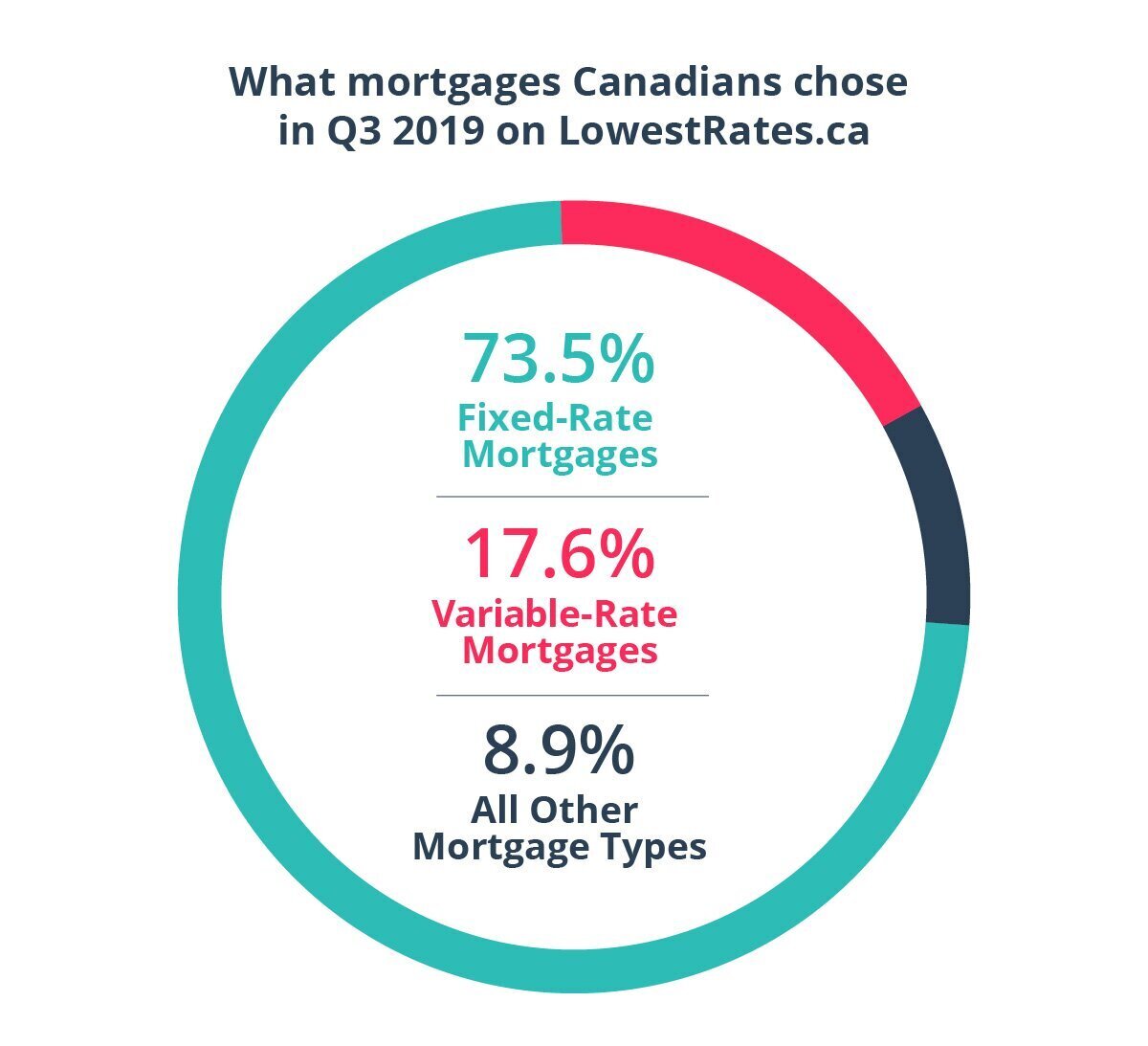

The data shows that, 73.5% of the quotes that were completed using LowestRates.ca’s mortgage quoter in the second and third quarters of this year were for five-year fixed rate mortgages, compared with just 17.6% for five-year variable-rate mortgages (the remainder percentage was for shorter terms, such as one or two year mortgages).

These findings are surprising, considering that historically, most people come to our site looking to compare rates on variable-rate mortgages. Since January 2014, we’ve seen an average of 56.56% of users going with a variable-rate mortgage, compared with 43.44% who chose a fixed-rate mortgage.

The dramatic difference recently suggests that there’s something weird going on in the world of mortgages.

Fixed-rate mortgages are cheaper. Here’s why

Back in July, we reported that fixed-rate mortgages were actually cheaper than variable-rate mortgages. At that time, you could find five-year fixed-rate mortgages on our site with a 2.41% interest rate, compared to a five-year variable mortgage with a 2.64% rate. That was highly unusual, given fixed-rate mortgages are almost always the more expensive option because they provide homebuyers with more stability. As a result, they typically feature a higher interest rate that doesn’t change (aka is “fixed”) throughout the entire term of the mortgage.

Variable-rate mortgages, on the other hand, don’t offer the same stability because they fluctuate with the market. When the Bank of Canada decides to hike or cut the overnight interest rate, for instance (which is the interest rate at which it lends money to banks), a variable-rate mortgage will likely be affected by either decision. While riskier, most people tend to opt for variable-rate mortgages for this very reason — over the course of their mortgage term, they could benefit from a lower interest rate for a period of time.

This mortgage inversion is still happening. As of this writing, the best deal on our site for a fixed-rate mortgage is 2.47%, compared to 2.64% on a variable-rate mortgage. So, the fact that our search volumes for five-year fixed rate mortgages were so high in Q2 and Q3 is indicative that people are still seeing fixed-rate mortgages as the safer bet.

Now, the last time we saw more people opt for fixed-rate mortgages over variable on our site was in 2018, when people were wary of higher interest rates. But does that fear still check out this time around?

How long can the fixed discount last?

The Bank of Canada hasn’t hiked or indicated it sees the need to hike interest rates for some time now. The overnight interest rate has remained at 1.75% since October 2018, when the bank last hiked it by 25 basis points. This year, economists have been calling for a cut, if anything, as the bank’s next move, though that forecast also seems to have softened. Still, many don’t expect a hike until the end of 2020.

It’s clear this time around, consumers are opting for fixed-rates because they’re simply cheaper. Why would you take the more expensive option, especially when it comes with more risk?

But this situation isn’t expected to last. While fixed rates have come down in expectation of a rate cut, that rate cut might not happen anymore — and if the market expects rates will start rising again, we could see the variable premium disappear.