REPORT: How COVID-19 changed Canadian car insurance shopping habits

By: LowestRates.ca Staff on June 10, 2020

When Canadian politicians began mandating the closures of restaurants, schools, daycares, and countless non-essential businesses in mid-March because of COVID-19, something very impactful happened: people stopped driving places.

In traffic-heavy cities, the deserted streets probably looked like something out of an apocalyptic thriller. For the first time in a long time, there were far fewer cars on our roads. This new reality continued well throughout the month of April, and even into May. Not only was it a pleasant side effect of a not-so-pleasant pandemic, it also changed the way Canadians shopped for car insurance, according to new LowestRates.ca data.

Consumer search interest for car insurance fell off a cliff in March during the early days of the COVID-19 shutdown, which had an effect on the overall number of quotes completed on our site. But then we started to see some interesting car insurance shopping habits emerge in the following weeks and months as the number of consumers visiting LowestRates.ca returned to normal.

See below for some key insights and analysis.

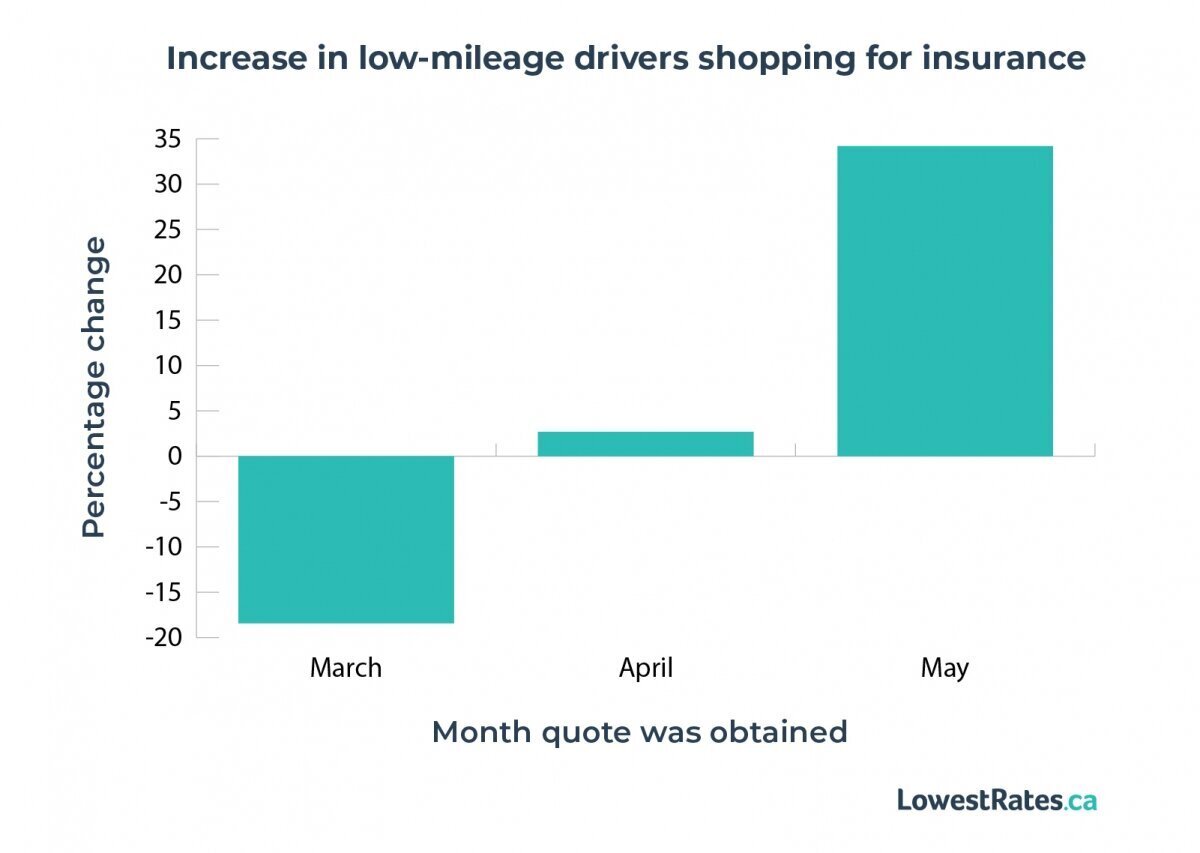

Increase in low-mileage drivers shopping for auto insurance

With most Canadians no longer commuting or using their vehicles as often when the lockdown measures were first introduced, there was a significant decrease in how much Canadians were driving.

As a result, we saw an increase in low-mileage drivers (people who drive fewer than 5,000 kilometres a year) shopping for car insurance on our site during March, April, and May.

Our data revealed that from February to March, there was a 3.54% increase in low-mileage drivers shopping for insurance. And from March to April — when lockdown measures were fully enforced — there was an even bigger jump, of 30.07%.

In fact, we’re still seeing the numbers trend upwards. The number of low-mileage quotes completed on our site increased again in May by nearly 6% month-over-month, and by 34.21% year-over-year.

One thing these low-mileage consumers may have benefited from during this time is cheaper insurance rates.

“Premiums are affected by vehicle usage and annual distance driven,” says Elektra Hilton, Director of Operations at DirectRate.ca, an insurance brokerage in Windsor, Ont.

“Customers who are driving less during the lockdown have the option of amending their vehicle use — from business/commuting to pleasure use — and the associated annual mileage, in order to lower their premiums. Alternatively, they also have an option to suspend coverage if a particular vehicle is not being driven at all. This would result in cost-savings as well.”

Mileage is just one of the factors used to calculate your car insurance premium. Insurance companies also take into account your age, your sex, where you live, your claims history, and the car you drive. Typically, low-mileage drivers can benefit from lower insurance rates because premiums are based on risk. From an insurance company’s perspective, the further and more often you drive, the more likely you are to be involved in an accident and need to make a claim. Therefore you’re seen as a higher risk to insure, and as a result, might face higher premiums.

As fewer people work from home and social-distancing rules become less strict, peoples’ mileage will inevitably increase again.

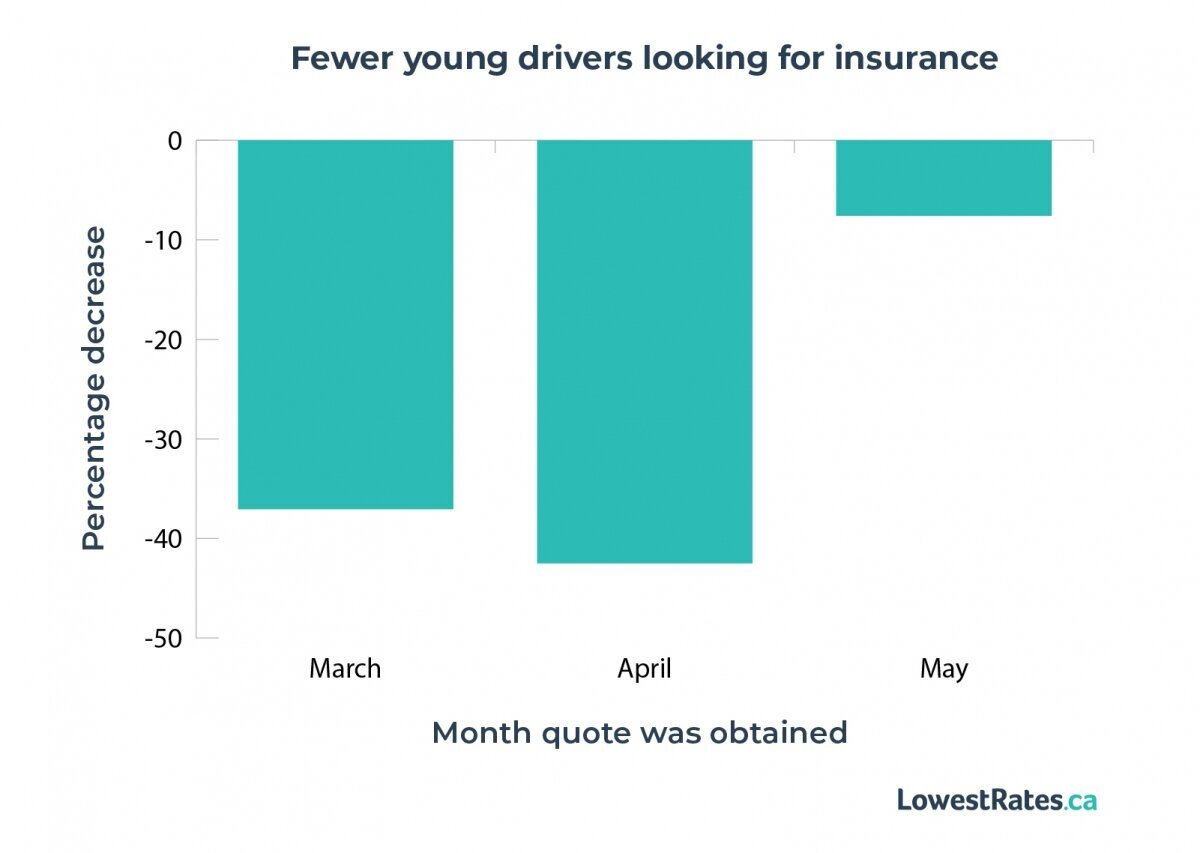

Fewer young drivers shopping for auto insurance

The lockdown also had an effect on young drivers and their search for auto insurance.

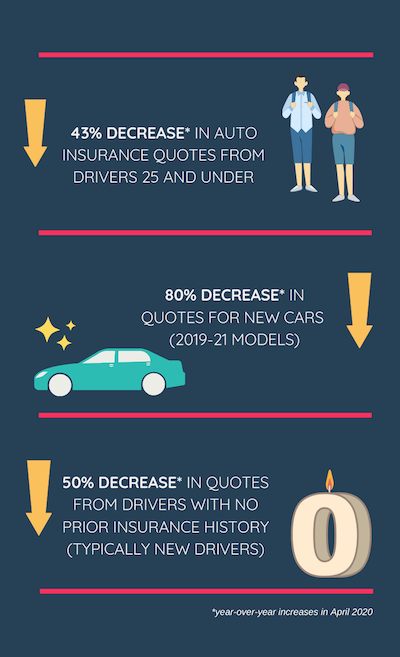

According to our data, the number of drivers under the age of 25 searching for car insurance on our site decreased. For instance, we saw the number of 25-and-under drivers drop by 3.90% from March to April. When we compare April of this year to April 2019, this is a 42.51% drop.

Driving examination road tests weren’t happening for much of March and April (and in every province except for Saskatchewan, still aren’t) due to physical distancing rules, so it’s likely that fewer novice drivers were hitting the market for a new vehicle and accompanying insurance.

The number of 25-and-under drivers using our site has increased significantly since April, however, with a 30.05% month-over-month spike in May. As dealerships slowly began reopening (many by-appointment-only) across the country, there’s a good chance that younger drivers are looking into buying and insuring their new vehicles.

Decrease in drivers with no prior insurance history

Similarly, the number of drivers with no prior insurance history (or those who had a gap in insurance) who obtained a quote on our site decreased in March and April, by 8.99% and 19.98%, respectively, month-over-month.

Year-over-year, we saw a 34.13% decline in March and a 50.24% decline in April.

This is likely evidence, again, of newer drivers (who typically don’t have any prior insurance history) not searching for insurance policies, since their ability to purchase a vehicle during the height of the pandemic was hindered.

We saw this number increase, however, by 45.32% from April to May, right around the time when many dealerships reopened, indicating that those with no prior insurance history (i.e. new drivers) were searching for an insurance policy again.

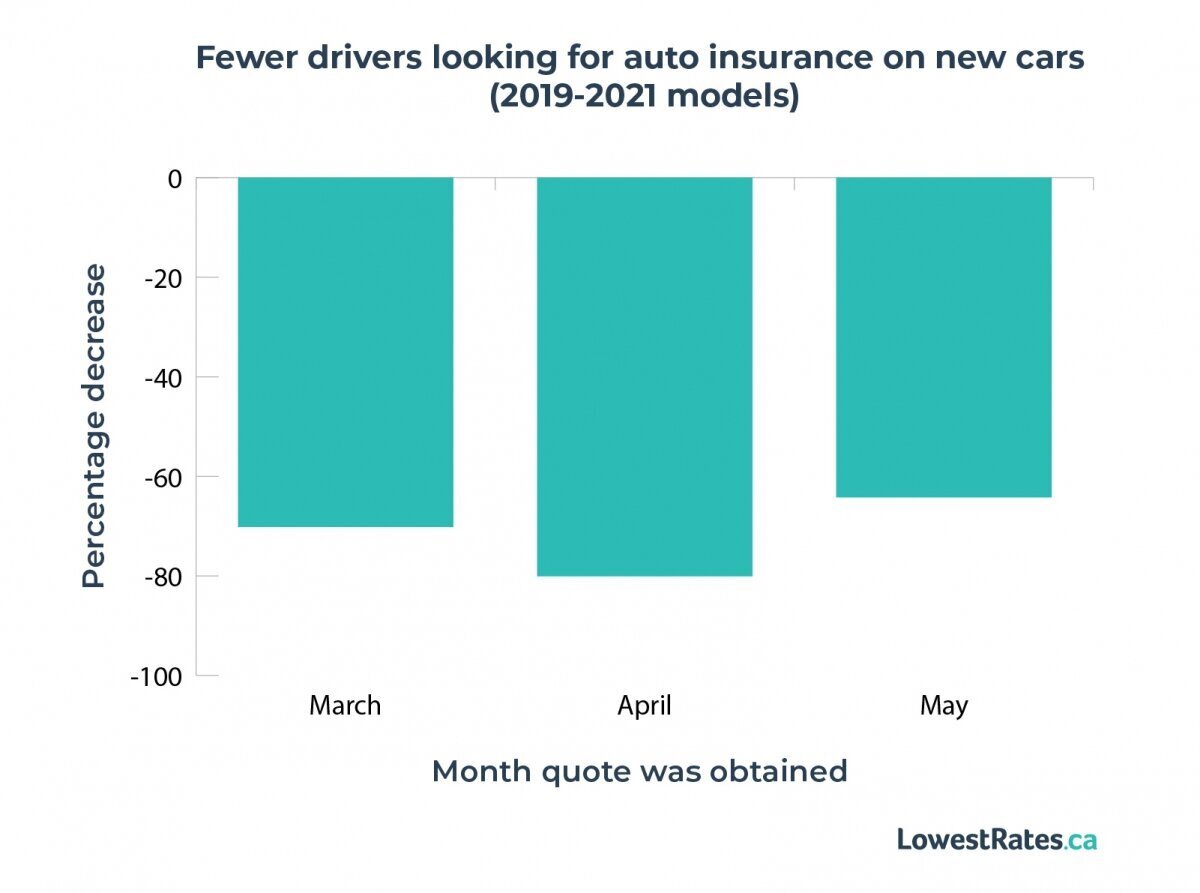

Fewer drivers searching for insurance for new cars

With most dealerships closed through much of March and April, it was considerably harder to buy a brand new car. Customers could purchase vehicles online or via email but they were unable to go into the showroom and test-drive new vehicles — both important parts of the vehicle purchasing process. Naturally, car sales plummeted.

That’s reflected in our data, which show that the number of individuals seeking car insurance quotes for new vehicles (2019-2021 models) dropped by 2.20% in March and 24.30% in April, month-over-month. Year-over-year, we saw a 70.17% decline in March and 80.08% decline in April.

This effect was felt by brokers, too.

“There was a noticeable decrease in consumer requests for auto quotes and new policies in April,” says Hilton. “With showrooms closed, consumers were unable to test drive or purchase new vehicles which, along with the uncertain economic situation, had an impact on insurance.”

This decrease didn't last for long, though. In May, we saw a 51.07% month-over-month surge in the number of people looking for car insurance quotes for new vehicle models (though the numbers are still down by 64.22% year-over-year). This is likely because many car dealerships were allowed to fully reopen in May, albeit, with guidelines.

Key Findings:

- The number of individuals that completed quotes on our site with low annual mileage (under 5,000 km) increased by 30% in April from the month prior, indicating that people were driving far less due to the lockdown.

- The number of individuals under the age of 25 who filled out quotes on our site dipped by 37% year-over-year in March and nearly 43% year-over-year in April, suggesting that young drivers perhaps looking to insure their first vehicle were unable to do so since car dealerships across the country were closed.

- The number of individuals obtaining quotes for auto insurance for new vehicles (2019-2021 models) decreased by 80% year-over-year in April, when most dealerships were closed and increased by 51% month-over-month in May when many dealerships across the country were allowed to fully reopen.

- The number of individuals with no prior insurance history obtaining quotes for auto insurance decreased by 50% year-over-year in April. Those with no prior insurance or a gap in their insurance history typically represent new drivers.