Ride-sharing in Canada: It's Complicated

By: Dominic Licorish on August 1, 2016

Before smartphones, ride-sharing was a bit like carpooling. Let’s say I was going to Montreal and I had a few extra seats in my car. Why not fill those seats with (non-threatening) people and cover my gas expenses on the ride? With the help of your network and maybe a ride board at uni, you could fill your car.

Today, thanks to the emergence of ride-sharing apps on smartphones, it’s become a massive, disruptive business that’s caused international headlines and uproar. Hailing a ride is as simple as a few taps on your phone and anyone with a car can effectively become a cab driver.

Judging by the amount of coverage it has received, you might think ride-sharing is disrupting taxi drivers all over the country. The truth is that Canada’s ride-sharing market is actually quite small. Lowest Rates whipped up a little something to give you a complete look at the ride-sharing industry in Canada -- and answer a few questions:

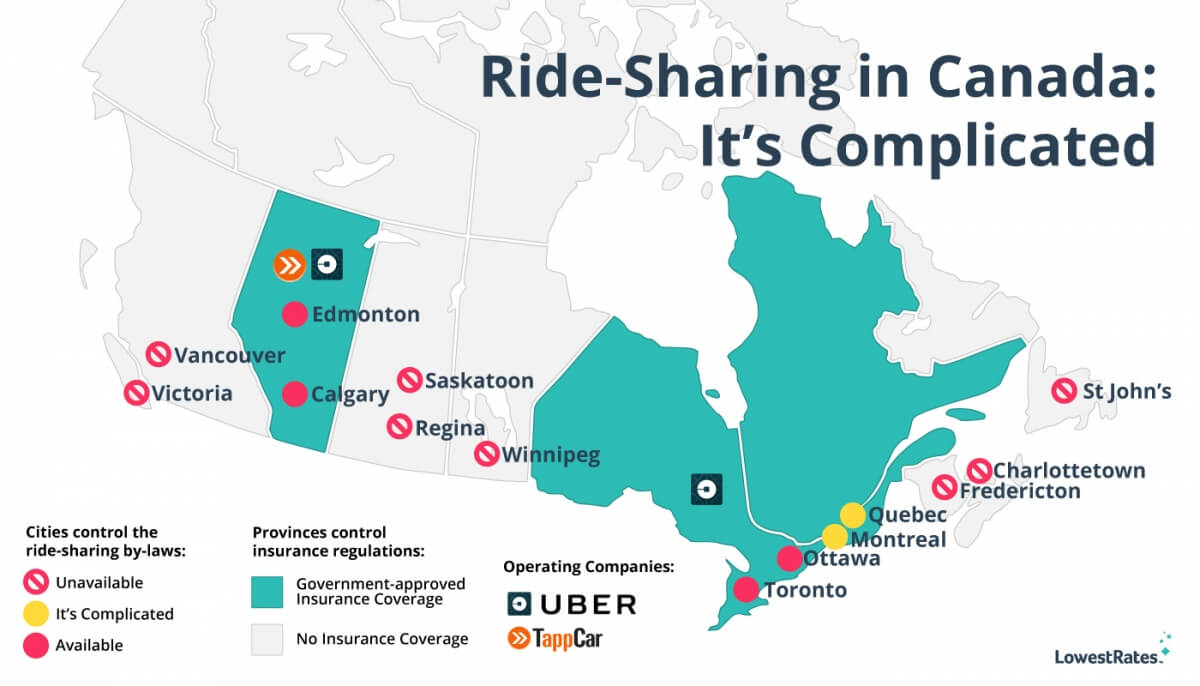

How many cities allow ride-sharing?

Right now there are only 14 areas in Canada with active ride-sharing services:

Calgary

Edmonton

Toronto/GTA

Ottawa

Montreal

Quebec City

London

Guelph

Waterloo

Kitchener

Niagara

Windsor

Hamilton

Kingston

While these cities make up about half of the country’s population, it’s pretty clear to see that geographically, ride-sharing has yet to spread throughout the country. It’s still very much an urban service, mainly available in major population and tourist centres. Thus, it’s no surprise that most of Uber’s network is in southern Ontario and Quebec.

TappCar is currently the only “transportation network company” (or TNC, the term people came up with for ride-sharing companies) in the country aside from Uber. It operates in Edmonton and Calgary.

So, is ride-sharing legal in Canada?

The answer is still confusing, but luckily it’s getting simpler as time goes on.

When Uber first came on the scene, no one really knew how to handle it. Not only were there no bylaws that applied to it, but car insurance policies didn’t offer the right coverage for Uber drivers. Personal coverage doesn’t really apply since drivers are earning money and cars are being used for commercial services. But ride-sharing drivers aren’t licensed as taxi drivers and that specific coverage doesn’t apply, either.

Ride-sharing coverage annoys many taxi drivers because they have to compete with a company that skirts the system and hurts their bottom line. Uber costs less than taking a taxi, and taxi companies and driver are lowering their own fares as a result. But it can cost more to become a licensed taxi driver and keep up with the insurance costs.

Taxi drivers did what any group of people do when they feel threatened: they protested. In the last couple of years, the Uber and taxi beef has reached comical proportions. The drama prompted politicians in most of Uber’s operating cities to work on approving or amending bylaws for taxis and transportation network companies (TNCs) that would satisfy both Uber and taxi drivers, as well as making sure citizens are as safe as possible.

Earlier this year cities began finally approving regulations for TNCs and putting an end to taxi protests. In Quebec, Edmonton, Calgary, Toronto, and Ottawa, bylaws have been passed defining rules for TNCs to follow. These rules are separate from the traditional taxi system, with some caveats. The ride-sharing laws in Quebec require Uber drivers to hold taxi permits, but it’s doubtful many of them will even attempt to get one. This problem comes down to enforcement, and it will be difficult to handle.

Government-approved insurance is mandatory when you’re behind the wheel, and many people agree that driving without insurance is stupid. However, Uber changed things. With regular folks suddenly driving people for money, people began asking questions about how insurance companies would handle ride-sharing. When companies made it clear that standard policies would not cover ride-sharing, it became something of a race to see which companies and what provinces would approve coverage first.

Unsurprisingly, with most of the ride-sharing population, Ontario ended up being the first with an approved ride-sharing policy, though it was only a policy extension through one company. Coverage has since spread to other areas of ride-sharing activity, first with Quebec and now Alberta, which made history last month by being the first province to approve a new insurance policy form so that TNCs could insure all of their rides themselves.

Blanket coverage is active now in Alberta and Ontario. For the first time, the majority of Uber rides are now properly insured, marking a huge shift in the legitimacy of the ride-sharing business.

What’s next for ride-sharing?

With the hurdles to ride-sharing removed from most of Canada’s big cities, expect Uber to expand to new markets such as B.C. (Technically, ride-sharing is already available in B.C., even though it’s not recognized as legal by the authorities.) Look for more transportation network companies to pop up soon, like DriveHer, which plans to launch this year in the GTA.

Ride-sharing has disrupted an industry that had remained unchanged for decades. Disruption brings innovation and a better experience for consumers. Ride-sharing may have had a rough start, but now that it’s here, it’s here to stay.