Why I don't want a mortgage

By: Nelson Smith on July 24, 2015

After almost a year abroad, I’m back in Canada. Once I got the important stuff out of the way -- like eating my weight in delicious foods that I missed -- my girlfriend and I came to an important realization. We needed a place to live.

We had a couple of options. We could stay in a relative’s place for next to nothing. Or, we could rent or buy something on the open market. Here’s what we did.

The selection process

Up until a couple of years ago, I’d always been for owning real estate. I liked the idea of having a permanent place to call my own. I liked the idea of being free to paint the walls whatever color I’d like. And I was all for finding a place we could call home forever, avoiding the inevitable pain of moving.

But then I spent a couple of years renting, and realized those were pretty silly things to get all worked up about. Besides, renting has quite a few advantages too -- like being able to leave practically on a whim or being able to put my money to work in investments, and not spending it on a new roof or siding.

Still, we decided to take a look at houses in our new town. We set a budget between $200,000 and $250,000, phoned up a Realtor, and had a look. Our new home isn’t so big, so there were about 20 houses that potentially had everything we were looking for.

And out of twenty, we agreed that we both liked two. One had an offer already on it, and the other needed a potential $10,000 worth of work to make the basement nice. The extra work would have put us above our budget, so we ended up passing on both.

Instead, we found a beautiful apartment for $1,550 per month. It’s in a brand new building, has two huge bedrooms, five appliances, and a terrific balcony where I’m currently sitting. Oh, and it includes all utilities, including internet.

Plus, it’s cheaper

With our new apartment, we’ve locked in $1,550 per month in monthly living costs. Let’s see what I’d pay if I bought the $250,000 house that needed $10,000 of work.

Say I put down 5% on the house, spending the rest to do the repairs. Based on a five-year fixed rate of 2.99% and CMHC fees, I’m looking at a monthly payment of $1,160 for the next 25 years. I doubt the payment stays that low for the next 25 years, but let’s go with it.

But there’s more. Because my new apartment includes utilities, I’m looking at an additional $500 per month for power, gas, water, and internet (cable is excluded for both). I’m also saving $200 per month in taxes, $75 per month in home insurance, and we’ll say $100 per month for home maintenance. Hey, a new roof isn’t cheap; neither is a kitchen renovation.

Add that all together, and I’m looking at a cost of $2,035 per month to own. Let’s round up and say it’s an extra $500 per month to own a place compared to renting.

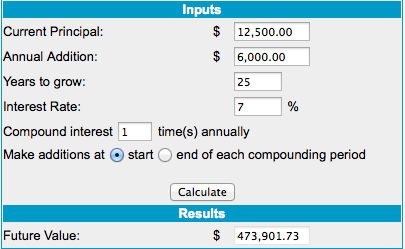

Now let’s assume I can invest that extra $500 per month (along with the original $12,500 down payment) at 7% annually. How much will I end up with at the end of the original 25 year mortgage.

For me, the choice was easy. I’m willing to rent for as long as it takes until it’s cheaper to own compared to renting. It’s the same in Toronto, Vancouver, and many other places. The math is simple, it’s a much better deal to rent.

.jpg?itok=SnQQgxS0)