Meet the creator of a new app that’s revolutionizing allowance for kids

By: Vin Heney on December 13, 2016

Are kids in Canada getting the right money message?

This past November, which was Financial Literacy Month in Canada, Ontario’s Ministry of Education announced that it would begin introducing financial literacy skills in Grade 10 careers courses.

A promising step in the right direction, but not everybody thinks it’s enough.

Alex Fung, Founder of Dollarwise, feels strongly that financial education is falling short. We spoke with him about why he thinks a “fun” app can change the future of finance for young Canadians.

Q: Tell us a little bit about yourself.

I used to work at Scotiabank and Fidelity Investments as a financial analyst, keeping track of sales teams, commissions, expenses, etc. So I have a good understanding of how mutual funds work in Canada. I began to realize that many Canadians weren’t benefitting as much as some individuals within the current framework, so I decided to leave my job and start my own initiative to help resolve some of those issues. Speaking with many Canadians, I heard people say ‘I wish someone had told me this earlier’ or ‘I don’t know how much it costs for someone to manage my mutual funds’. It was a really big problem. Many parents told me ‘I just wish someone taught this to my kids in an engaging way.’

Q: Why is financial literacy important to you?

It started when I was 8 years old. I decided to buy a video game without my parents’ permission. When I brought it home, they were furious and kicked me out of the house in the middle of the night. My brother eventually convinced me to go back inside and figure out why my parents were so mad. Turns out it was because I’d made an impulsive decision with my money. So that traumatizing experience is what led me to study and work in finance. But I started realizing Canadians had the same problems I had as a kid, and the current solutions weren’t working. So that’s why I’m passionate about the problem.

I was 8 years old. I decided to buy a video game without my parents’ permission. When I brought it home they ... kicked me out of the house.

Q: What is Dollarwise? Why develop an app?

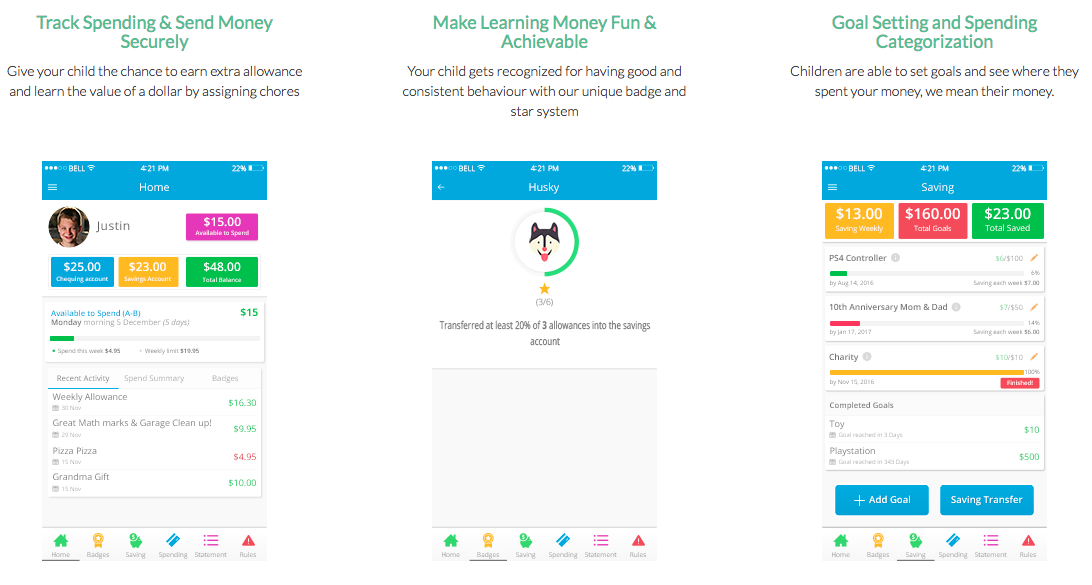

We help parents teach their kids good money habits using a debit card and a mobile app. Unlike a traditional institution, we want to make it fun and meaningful for kids, so we ‘gamified’ the experience by using allowance and tied it into savings, spending responsibly, earning, and even giving. In personal finance, it’s not really talked about much — being able to give when you’re in a position to. So we’re essentially trying to get rid of cash allowance so that parents and kids are able to track their spending and saving habits. The problem with cash is that if kids lose the money it’s gone forever, and it’s difficult to track behaviour. With a debit card, we’ll track it for them, allowing parents and children to speak to one another about money. Actually, money is a taboo topic in many households; we’re trying to enable it to lead to conversations.

Q: Have any kids tested the app? What was the feedback?

In the beginning, it was targeted towards millennials, but a lot of them didn’t care much. We found there was a bigger demand among parents and children. ‘Start ‘em young’ is the motto! Based on the latest version, the feedback has been pretty positive. Although many parents still give cash allowance, it’s becoming increasingly inconvenient. So when I mention that you can use your banks to give kids allowances with their debit cards, there’s usually good interest.

Q: What have the reactions been like from the big banks?

A lot of them like it. I’ve also been speaking with several smaller financial institutions and they’re actually more interested. So the feedback has been positive from both ends. It’s just that I wasn’t looking forward to waiting the average of 18 months that banks were saying it would take to implement the idea. I wanted something quicker, but that still has high impact.

Q: Do you hope to implement Dollarwise across the country?

Absolutely. It’s not restricted to one institution. I think every Canadian child should have access to this educational tool. There are pros and cons of Canada being behind other countries in terms of technology. I’m finding that the tech companies in the UK tend to be advanced, and the citizens are early adopters. The great thing about that from the Canadian perspective is that we can see the results and the impact on users, such as children asking their parents to do more chores and help out more around the house.

Q: So this technology is essentially creating young entrepreneurs?

Yeah, pretty much!

I wish someone had told me this earlier

Q: What was the hardest part about developing Dollarwise?

The most challenging part was the multiple iterations of the prototype. We’re currently on the fourth iteration. The first one wasn’t user-friendly and the interface wasn’t that nice. For the fourth version, we made it a lot more kid-friendly. We have two core users essentially: the kids, which are eight-to-15, and the parents, which are about 38-to-48 years old. So designing something for two different groups of users was the most challenging part.

Q: Do you plan to monetize Dollarwise? If so, how?

Yes, but it’s more of a value-add for institutions, so revenue would not be coming out of children’s or parents’ accounts. It’s more a tool for parents to help them teach their kids good money habits. The institutions get to reduce the acquisition and retention costs of new clients and they’re able to promote that they’re pro financial literacy in a way that’s innovative and engaging. But honestly, if I was in it for the money, I would’ve stayed at my previous job. It’s not really about the money for us, it’s about making a difference.

Q: When do you expect it to be available to the public?

It depends on a few variables, but I’m expecting middle or late 2017. We’re still testing our prototype and getting feedback.

Q: What do you see as lacking in Canada’s current approach to financial education?

The Ministry of Education in Ontario is mandating that financial literacy be taught. The problem is that it’s starting too late. They’re incorporating it into Grade 10 career classes, but habits have already been formed as young as 10, even seven years old. There’s a lot of pressure on purchasing products and services at a young age. There are also a number of financial literacy workshops offered across the country, but the problem is that there isn’t constant reinforcement. These workshops tend to be during Financial Literacy Month, and kids forget quite easily. If kids aren’t engaged, they’re less likely to retain the information and can easily revert to media and peer pressure.

[W]e want to make it fun and meaningful for kids, so we ‘gamified’ the experience

Q: Finance can be confusing and boring! How did you go about designing an app that appeals to youth?

The challenge is making it fun. We spoke with children and tried to understand the most successful products in the market right now — not just in terms of financial literacy, but in general. So we needed to make something fun, educational, and parent-approved. Trying to teach financial literacy in school doesn’t really work, workshops aren’t long-lasting, and so understanding how apps are effective is all about understanding what’s fun and engaging.

Q: What are your thoughts on the FinTech space right now in Canada?

I think the FinTech space in Canada is great, it’s just that nobody’s really focusing on the younger generation. I think that’s a big gap and a big opportunity.

Q: Are you looking for seed funding?

Honestly, we’re not. We’re trying to find an institution to help fund the development of the app. Then after that, we want to white label it for institutions because they already have loyal customer bases and strong brands. Then we can look to start raising fee funding. But right now, we don’t want to jump into it prematurely.

Q: What’s your #1 personal finance tip?

Save your money!

*Dollarwise is currently inviting the first 1000 households to respond to a brief online survey and an opportunity to test the application prototype.