Credit Cards

Credit CardsHow secured or guaranteed credit cards help fix bad credit

Key takeaways: Secured credit cards are the simplest and most accessible option to improve bad credit or...

Find the right credit card.

Get StartedFocus On

Comparing rewards credit cards can be confusing for even the savviest consumers. Most rewards cards offer different rewards rates depending on the amount of money you spend and what exactly you spend it on. Just take a look at the Scotia Momentum Visa Infinite.

With this card, you can earn 4% cash back on eligible gas and grocery purchases, 2% cash back on drugstore purchases and recurring bills, and 1% cash back on other purchases — up to a maximum of $25,000. After you hit this spending threshold, the card returns 1% cash back on eligible purchases.

Check out the rewards rates and benefits on some of our top cash back cards below:

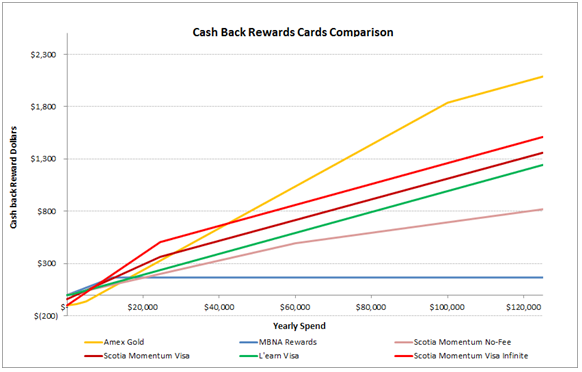

That’s a lot of math. We even crunched some numbers to illustrate what kind of rewards you’ll earn on each card based on the amount of money you spend. The graph below depicts the rewards rate for some of our best cash back credit cards — the most popular rewards category at LowestRates.ca.

A quick note on methodology: cash back rewards rates vary based on what you buy, so we used a weighted basket to depict the average cardholder's monthly spending.

We used a basket of up to $60,000 in spending, beyond which all purchases are categorized as ‘other’. Most families only spend so much money per year on items like gas, groceries, and recurring bills, no matter how big their budget.

We also included the annual fees for each card and stripped out introductory offers. Now you can get a true sense of how each card will reward you over the long term.

While every family spends money on different things and in different amounts, the graph above gives you a rough idea of the rewards you can earn with these cards based on your annual spend.

Figuring out which card will give you the best rewards rate depends on how much you spend per year. No fee rewards cards like the L’earn Visa or the Scotia Momentum No-Fee are actually better if you only spend a few thousand dollars per year on your card. If you’re a big spender, a Cadillac offering like the Scotia Momentum Visa Infinite reigns supreme.

50+ trusted partners (and growing) on our site to compare mortgage rates, insurance and credit cards

$1 billion+ saved in interest and fees

14+ million Canadians helped per year

Looking for more credit card info? Check out our Help Centre.

The competition for new credit card customers is intense, so credit card providers offer robust rewards programs to entice shoppers and get them to use their higher end cards.

Some cards offer travel points toward airfare and hotels, some offer points toward your favorite retailers, and others offer cash back. Just pick the rewards card that fits your spending habits and your lifestyle.

Wondering when you get to redeem those rewards? Rewards credit card providers generally award points monthly or once a year, and then you can redeem your rewards online or over the phone whenever you're ready. Meanwhile, cash back awards usually come in the form of a cheque at the end of the year or as a credit to your account. Just remember: the more you spend, the greater your rewards.

Consumers with good credit scores and average or above average credit card spending. Many rewards cards come with high annual fees and high interest rates, which is why they're best for shoppers who pay their balances every month and spend enough money to make the annual fee worth it.

You also need a reasonably high income to get approved for a rewards credit card. In most cases, rewards credit card providers require you to have a minimum household income of $35,000 per year. Other rewards cards require applicants to have annual incomes that are as high as $100,000.

Figure out what kind of rewards suit you best. Most shoppers start by looking at what they spend their money on each month and what kind of rewards would be most useful. Frequent travellers probably want a card with a travel points program, such as air miles or hotel points. High spenders might prefer cash back, while consumers with special interests may want a specialty rewards card.

The key measure of a rewards credit card is how much cash back or how many points are awarded per dollar spent. This measure is known as the rewards rate, or, sometimes, the rewards ratio.

The best rewards credit cards return at least 1% of your monthly spending back to you in rewards, whether it’s cash back, points, or another benefit.

Look for cards with reasonably ‘clean’ rewards programs — cards that don’t put a lot of limits or conditions on how you can earn and use your rewards.

And consider the annual fees — some rewards cards have annual fees over $200. But don’t just dismiss these cards, especially if you’re a big spender. These rewards cards may come with sign-up bonuses and a great rewards return rate.

APRs on rewards cards can be 20% or even 30%, and the annual fees can amount to hundreds per year. That’s why most rewards credit cards (especially premium offerings) are only appropriate for consumers who spend a lot of money.

Applicants also need to have a good credit score to be approved for a decent rewards credit card. Most rewards cards require a minimum score of 710, and the threshold is even higher for premium cards — usually 720 or above.

Check for caps or limitations on your rewards. Many rewards cards only offer the best points rewards rate on the first few thousand dollars you spend. When you exceed that annual amount, you're subjected to a lower rewards rate. Other cards come with a hard cap, beyond which no more rewards points will be awarded, no matter how much you spend.

You also need to check for requirements or conditions on your rewards. Some high-end rewards cards require you to spend a lot before you can get the best rewards rate. That's why many shoppers opt for a rewards credit card with a steady rewards rate and few variations.

Make sure your spending habits match the rewards card you're interested in applying for. Some rewards credit cards only offer points or cash back on certain products or services. That's why you should take the time to calculate how much money you actually spend in each of those categories before you apply for the card. For example, if you don’t own a car, a rewards card that earns cash back on gas purchases probably isn’t the right fit.

And lastly, remember to watch out for rewards that expire at the end of the year or after a set period of time.

LowestRates.ca may receive compensation when you click on links to those products or services; however, our content and calculations are objective and free from bias. The opinions expressed are purely those of LowestRates.ca; thus, partners are not responsible for any editorials or reviews that may appear. For current term and conditions on any advertiser or partner’s product, please visit their website.

Credit CardsKey takeaways: Secured credit cards are the simplest and most accessible option to improve bad credit or...

Credit Cards

Credit CardsThis article was last updated February 2026. If travelling is your passion, a travel rewards credit card can hel...